FOR THOSE WANTING to acquire or flip businesses

Add: How I flip & Acquire businesses for a living ”part-time”, without using my own money

Find your first 3 business acquisition targets in 48 hours using AI..... without brokers, databases, or cold calls.

What is "Close First AI"?

The Close First AI Deal System is a smarter, more leveraged way to find, analyze, and close profitable businesses automatically without spending hours hunting for leads, guessing valuations, or managing endless spreadsheets.

You don’t need to be a finance expert, have a massive network, or know how to structure a deal from scratch.

Instead of manually sourcing sellers and sending hundreds of cold emails, you can install our plug-and-play AI deal system.

Here's how it works:

This is the Close First AI Deal System.... Built for freedom, focus, and results.

It’s powered by automation, not exhaustion.

Designed to help you source, analyze, and close profitable deals without spending your life chasing them.

I created this system to replace the stress of manual deal flow with something smarter, faster, and proven.

This isn’t theory or guesswork.

It’s a practical, repeatable process that works around the clock to bring you qualified opportunities and help you close with confidence.

Limited Time Only:

Only $27 Today

(Save $270 today)- Delivered to your inbox within 60 seconds..

100% secure 256-bit encrypted checkout

Backed by Our 100% Money Back Guarantee.

Here's Everything You Get for Just $27:

Total Value: $1,297+

Close First AI Starter Blueprint

Negotiation Strategies for Buying Businesses

Seller Outreach Frameworks

AI Deal Analyzer Demo & GPT

A-Z Step-by-Step Business Flipping Doc

BONUS: Private Bonus Training Vault

BONUS: New Private Community

BONUS: FREE Bonus Automations Training (Coming Dec 2025)

UPDATED BONUS FOR 2025: Analyze & flip Media Assets

Only $27 Today

60-Days Money-Back Guarantee

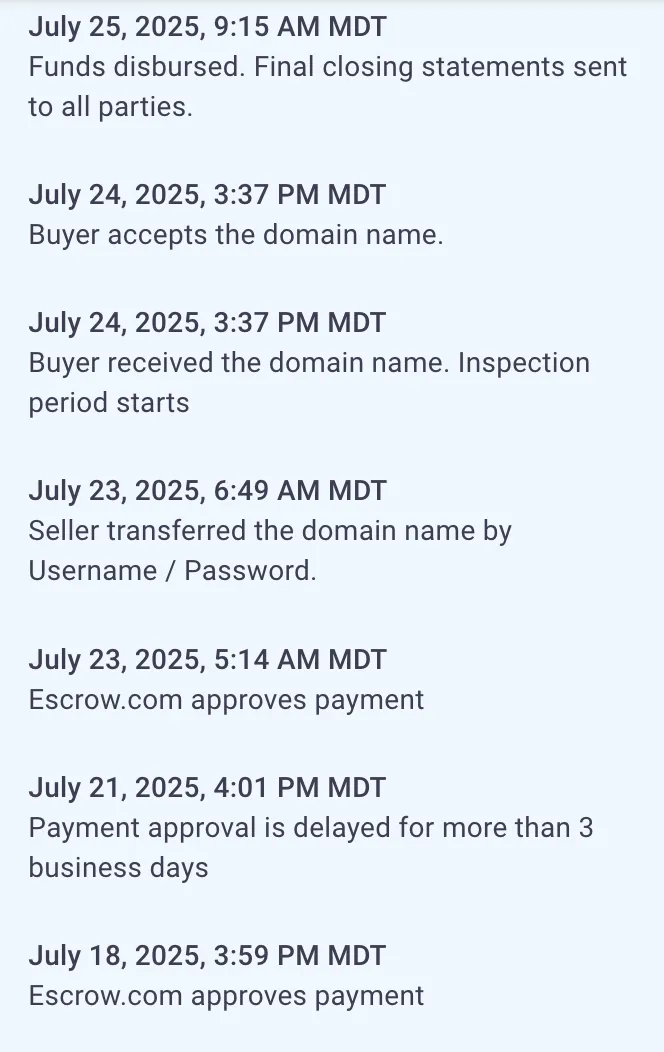

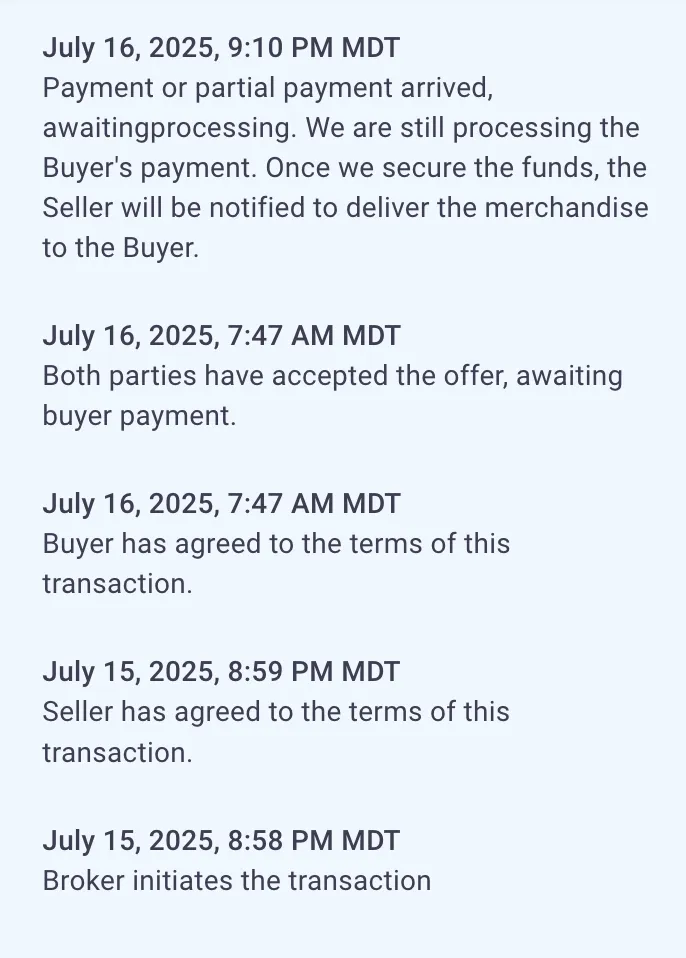

Another Deal

Escrow Closing Process

Why Close First AI

Enough Asking Yourself Where Your Next Customer Is Coming From...

I still remember the "income rollercoaster" season...

One day I'd find a solid deal and the rest of the week sometimes a month.... Crickets

Leaving me with all sorts of headache:

We spent 10 months and 60k on generic consulting to close our first deal

Nervous about bills piling up and not having any clear strategy to break through in my business...

Not knowing what targets to hunt and how to make offers & they will happily accept

Even worse...

Most buyers I talk to are finding a deal every 2 to 4 weeks. It looks good on paper, but there is no consistency. One week the inbox is quiet, the next week it’s chaos, then nothing again. Momentum dies, follow-ups slip, and the pipeline never compounds.

What changes with Close First AI:

Daily sourcing from multiple channels so leads hit your pipeline every morning, not once a month

Automatic follow-ups that revive silent sellers and keep warm conversations moving

Qualification rules that filter tire-kickers and flag real opportunities fast

A simple rhythm you can run in under an hour a day so deal flow stays steady

The goal is not random spikes. The goal is predictable deal flow you can plan around, with a clear path from first contact to closed.

All this to finally build a business I love with multiple revenue streams:

Go from finding a deal every few weeks to building steady, predictable deal flow every day

Eliminate the feast-or-famine cycle with automated sourcing and follow-up systems

Focus on closing qualified opportunities instead of chasing inconsistent leads

If you want real freedom, this is it.

I’m genuinely grateful I found a way to turn my deal-making process into a system that runs on its own.

Close First AI allows me to automate how I find, analyze, and close businesses, while new opportunities and income come in every single day.

It’s not complicated or technical. It’s a clear, proven system anyone can follow to build multiple revenue streams and recurring cash flow without constantly starting from zero or chasing the next deal.

The Close First AI Deal System has become more valuable to me than any material asset I own.

Because the peace of mind that comes from having predictable deal flow and passive income is priceless.

That’s real freedom to me — time freedom, location freedom, and financial freedom.

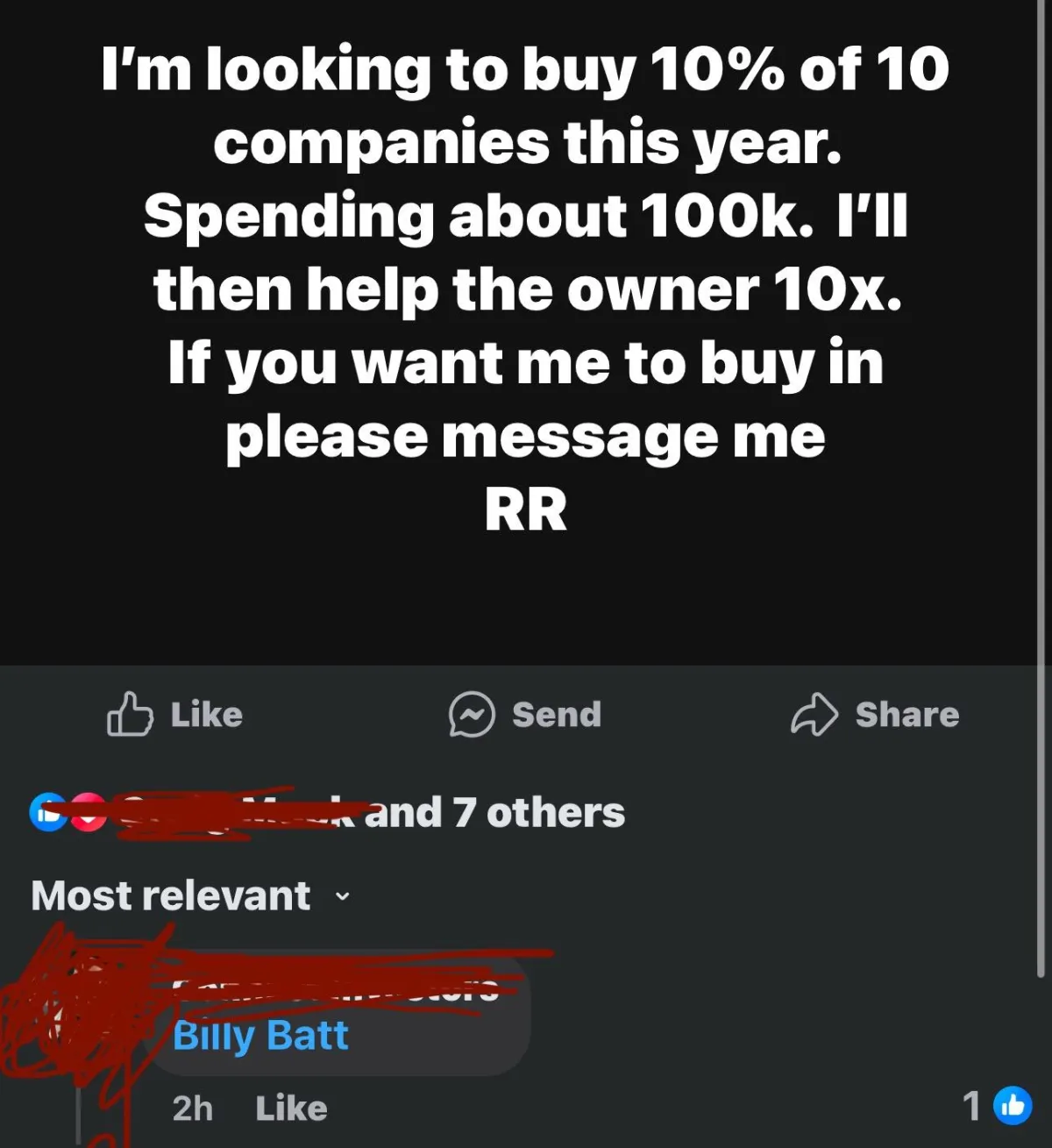

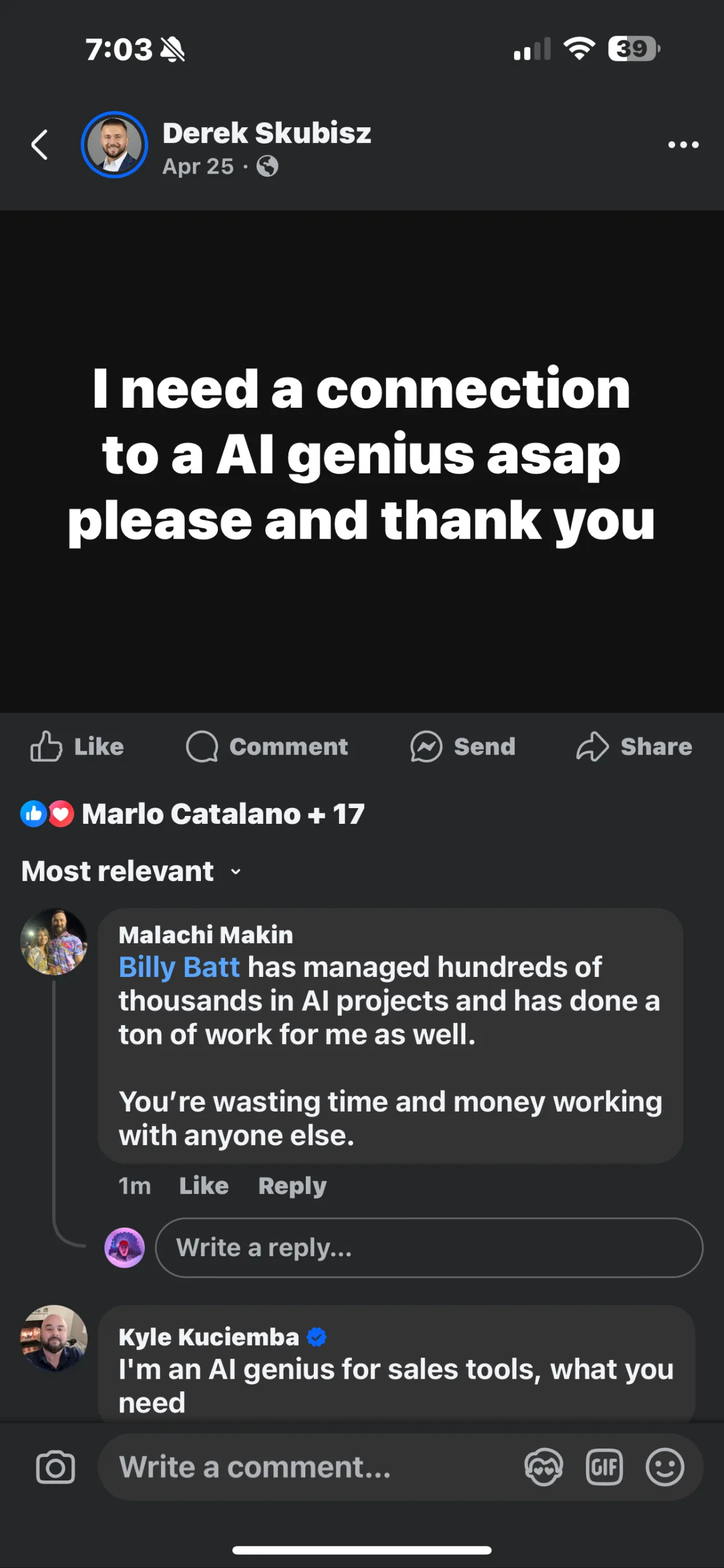

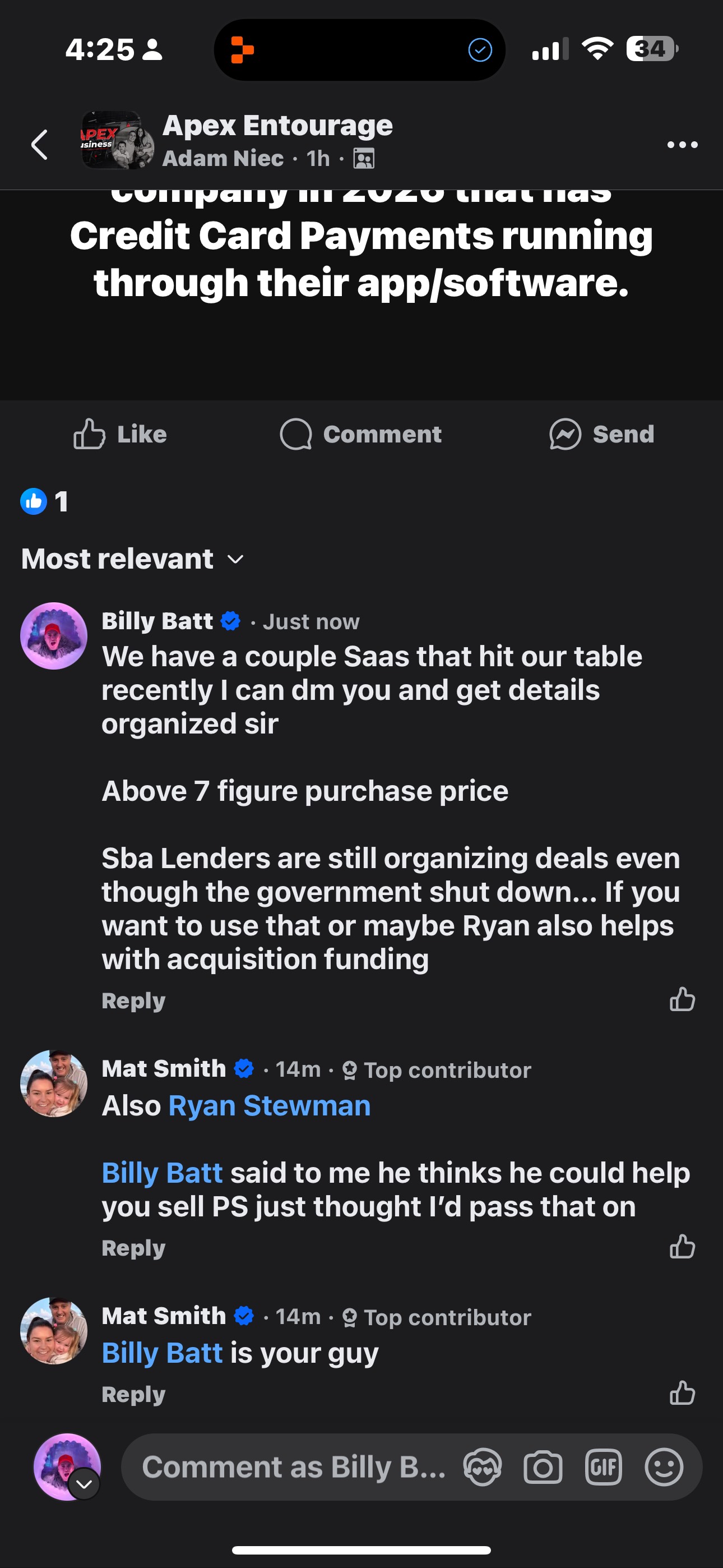

HERE'S PROOF THIS WORKS:

Get The Same AI Funnel System You Can Install Yourself:

Only $27 Today

(Save $270 today)- Delivered within 60 seconds..

100% secure 256-bit encrypted checkout

Backed by Our 100% Money Back Guarantee.

Some 2026 Results & Being Recommended

WHAT'S INCLUDED IN The BUNDLE

Here's Everything You Get Instant Access to For Just $27

Everything you need to launch your first or next high-converting automated sales funnel in minutes, using AI.

Close First AI Starter Blueprint

Learn the exact step-by-step system to use AI for finding, analyzing, and tracking small business deals fast — even if you’ve never closed one before.

AI Deal Flow Templates

Plug-and-play spreadsheets and trackers that help you organize leads, qualify sellers, and stay on top of every opportunity without getting overwhelmed.

Seller Outreach Frameworks

Proven AI-assisted scripts and message flows that get real business owners to respond and start deal conversations.

A-Z Deal Analyzer Demo

A simple walkthrough showing how to use AI to break down business listings, spot red flags, and identify profitable targets in minutes.

Private Bonus Training Vault

Mini-trainings showing how to scale your deal flow, build relationships with sellers, and position yourself as a serious buyer.

New Private Community

Get access to a members-only network of dealmakers, buyers, and acquisition entrepreneurs sharing live deal flow, AI setups, and real results. Stay accountable, ask questions, and connect with people closing deals just like you.

FREE Team Access

Add your team for free and hand off the implementation to team members or outsource it completely to save even more time.

Today Just $27

(Save $270 today)- Delivered within 60 seconds..

Backed by Our 100% Money Back Guarantee.

From the Oil Fields to the World of Deals

The Journey That Changed Everything

THIS IS ME IN 2016

In 2016, I was just a guy in the oil fields.

Running crews of 100 to 150 men. Covered in grease, dust, and fire every single day.

I’m a journeyman red seal pipefitter and welder by trade.

Twelve to sixteen-hour days. Seven days a week.

The money was good, but I knew something was missing.

When my daughter was born, everything changed. I realized I wasn’t chasing freedom. I was just trading time for paychecks.

That’s when I started looking for a way out.

I got into online marketing, lead generation, automation, and sales team building.

We made great money. But deep down, I still felt like I was stuck working inside a system that wasn’t mine.

Then 2020 came around, and that’s when I discovered M&A.

Mergers and acquisitions. The world of buying and flipping businesses.

It took 10 months and $60,000 of advice before we closed our first deal. Most of what we learned, we had to figure out ourselves.

But once that first deal closed, everything clicked.

We realized that online businesses were the smartest and fastest way to get started.

We began flipping them. Then we started buying our own. Ad tech. Software. Audiences.

And that’s when the mission became clear.

We didn’t just want to play the game. We wanted to help others learn it too.

Today, our team teaches entrepreneurs how to use AI and marketing systems to generate income while learning M&A.

We show them how to flip their first businesses.

How to build their own portfolios. How to create real freedom.

And we’re not stopping at online businesses anymore.

We’ve expanded into the medical space, applying the same systems and strategies that helped us grow from the ground up.

This isn’t about theory. It’s about execution.

It’s about creating time, money, and freedom through real business.

That’s what we do. And that’s why we’re here.

About Billy Batt

Billy Batt is a seasoned entrepreneur and leader at PAG, known for his disciplined approach to building scalable, results-driven businesses. With a strong foundation in strategy, execution, and accountability, he helps organizations simplify complex challenges and turn vision into action. Billy brings a no-nonsense mindset focused on growth, efficiency, and long-term value creation. When he’s not working, you’ll find him spending quality time with his daughter or pushing himself in the boxing gym.

OUR 100% MONEY BACK GUARANTEE FOR 30 DAYS

Try It Out & Get Your Money Back if You Don't Absolutely Love It

I'm so confident you'll love this system, so I'm willing to take the risk on me. Just try it out and if you're not completely satisfied with your results within 60 days, I'll refund every penny – no questions asked.

That's how certain I am that this will be one of the best investment you make in your business this year.

Frequently Asked

Questions

What exactly is the Close First AI System?

Close First AI is a plug-and-play system that helps you find, analyze, and close profitable small business acquisitions automatically. It combines pre-built AI automations, sourcing tools, and deal templates to replace hours of manual work with simple, guided workflows. You’ll discover how to build predictable deal flow, qualify sellers fast, and close profitable businesses — even if you’ve never done a deal before.

Who is this for?

This system is for entrepreneurs, acquisition beginners, dealmakers, and investors who want to build real wealth by buying or flipping businesses. It’s perfect if you want consistent deal flow, better quality opportunities, and more automation in your acquisition process.

Do I need to be tech-savvy to use this?

Not at all. Close First AI was built for non-technical entrepreneurs. You don’t need to code or integrate complex tools. Everything is plug-and-play, with step-by-step setup guides and preloaded automations that handle 90% of the work for you.

What do I get when I buy today for $27?

When you join today, you’ll get:

✅ The Close First AI Starter Blueprint — how to use AI to find and evaluate businesses fast

✅ Deal Flow Templates to organize and qualify opportunities

✅ Seller Outreach Frameworks that help you connect with real business owners

✅ Access to private bonus trainings that show how to scale into multiple acquisitions

You’ll have the foundation to start generating real deal flow — and when you’re ready, you can upgrade to unlock the full automation and backend systems.

How is this different from other AI tools?

Most AI tools just give you chatbots or prompts. Close First AI gives you a real-world framework built by dealmakers — so you’re not guessing how to apply it. You get the system and the strategy behind it.

How fast can I get started?

You can start today. Most users complete the setup and first sourcing workflow in under an hour. You’ll see exactly how to automate your first deal search by tonight.

Which softwares do you support?

The starter system runs on tools like Google Sheets, Notion, or Airtable — simple platforms you probably already use. You don’t need any special software or subscriptions. There will be hidden gems used specifically for Deal SOurcing

What’s the catch? Why only $27?

No catch. This is the starter version of Close First AI. It’s priced low so you can experience results fast and see how powerful the system is before moving into the advanced automation suite or mentorship.

What if I don’t like it?

You’re protected by a full 60-day money-back guarantee.

If you go through the system and decide it’s not for you, simply reach out within 60 days and we’ll refund every dollar. No stress, no questions asked.

You either build real AI-powered deal flow or you get your money back.

This site is not a part of the Facebook™ website or Facebook™ Inc. Additionally, this site is NOT endorsed by Facebook™ in any way.

FACEBOOK™ is a trademark of FACEBOOK™, Inc.

The information provided on this page and in our materials is intended for educational and informational purposes only. We do not make any guarantees about your ability to achieve results or earn money using our ideas, information, tools, or strategies. Your success depends on your own efforts, experience, and situation. We can, however, guarantee your satisfaction with our training: if you’re not completely satisfied, we offer a 60-day 100% satisfaction guarantee on our products—simply request a refund.

Any financial examples shared here are illustrative only and should not be considered average earnings, exact earnings, or promises for actual or future performance. Always exercise caution and consult your accountant, lawyer, or professional advisor before acting on any information related to lifestyle changes, business decisions, or finances. You alone are responsible for your decisions, actions, and results, and by registering or purchasing, you agree not to hold us liable for your choices or outcomes at any time under any circumstances.

This publication has been prepared without considering your individual objectives, financial situation, or business needs. Please assess whether this information is appropriate for your personal circumstances. To the maximum extent permitted by law, the publisher disclaims all responsibility and liability to any person for any action taken or not taken based on this information.

Copyrights 2026 | Closefirst.ai | Terms & Conditions